The year 2026 represents one of the most significant shifts in healthcare costs in recent memory. For both individual consumers and small employers, the landscape of monthly premiums and out-of-pocket expenses has been transformed by the expiration of pandemic-era federal provisions and new Medicare adjustments.

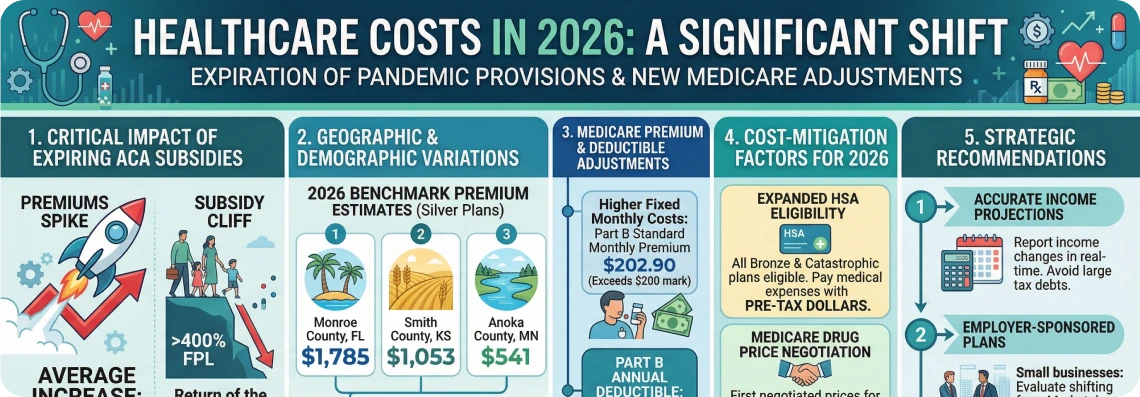

1. The Critical Impact of Expiring ACA Subsidies

The most influential factor driving premium estimates in 2026 is the expiration of enhanced premium tax credits originally introduced during the pandemic.

- Average Payment Spikes: For subsidized enrollees who stayed in the same plan, monthly premium payments are estimated to have increased by an average of 114%.

- The Return of the “Subsidy Cliff”: Households with an income exceeding 400% of the Federal Poverty Level (FPL) are once again ineligible for financial assistance.

- Removal of Repayment Caps: Starting in 2026, individuals who underestimate their annual income may be required to repay the full amount of excess advance premium tax credits (APTC) they received, as the previous caps on repayment have been eliminated.

2. Geographic and Demographic Variations

Monthly premiums for Marketplace plans vary drastically based on location, age, and family size.

2026 Benchmark Premium Estimates (Silver Plans)

For a 50-year-old individual, monthly premiums for the second-lowest-cost Silver plan (the benchmark plan) show wide regional gaps:

- Monroe County, Florida: Estimated at $1,785.

- Smith County, Kansas: Estimated at $1,053.

- Anoka County, Minnesota: Estimated at $541.

For a family of four in Monroe County, Florida, the benchmark monthly premium reached approximately 3,799∗∗.Acrossallexchanges,theaveragemonthlypremiumbeforetaxcreditsisestimatedat∗∗741, while the average after credits is $178.

3. Medicare Premium and Deductible Adjustments

Beneficiaries of Medicare are also seeing higher fixed monthly costs and deductibles due to rising medical care demands.

- Part B Premiums: The standard standard monthly premium for Medicare Part B rose to $202.90, exceeding the $200 mark for the first time in history.

- Medicare Deductibles: The Part B annual deductible increased to 283∗∗,whilethePartAdeductibleforinpatienthospitalstaysroseto∗∗1,736 per benefit period.

4. Cost-Mitigation Factors for 2026

Despite the general trend of rising costs, several new provisions offer opportunities for savings:

- Expanded HSA Eligibility: For the first time, all Bronze and Catastrophic plans on the Marketplace are now eligible for Health Savings Accounts (HSAs), allowing users to pay for medical expenses with pre-tax dollars.

- Medicare Drug Price Negotiation: In 2026, the first negotiated prices for 10 high-cost drugs (including Eliquis, Jardiance, and Januvia) took effect. These prices are at least 38% off the 2023 list prices.

- Drug Spending Cap: Yearly out-of-pocket costs for Medicare Part D prescription drugs are now capped at $2,100.

5. Strategic Recommendations

To manage these increases, experts suggest the following:

- Accurate Income Projections: Given the removal of repayment caps, reporting income changes to the Marketplace in real-time is essential to avoid large tax-time debts.

- Employer-Sponsored Plans: Small businesses are encouraged to evaluate shifting from the Marketplace to employer-sponsored coverage, which can provide more predictable cost structures.

- Supplemental Coverage: Medicare beneficiaries should review Medigap or Medicare Advantage options to help cover rising out-of-pocket costs and deductibles.

Fuente: Reuters

https://www.reuters.com/legal/litigation/obamacare-enrollment-drops-about-23-million-people-2026-2026-01-29/

Fuente: AARP

https://www.aarp.org/medicare/whats-new-in-medicare-2026/

Fuente: HealthInsurance.org

https://www.healthinsurance.org/blog/8-big-changes-reshaping-marketplace-health-coverage-in-2026/